Over the last five years, many law firms have reduced costs by slashing overheads and firing underperforming partners. Despite this, profit margins remain under pressure. Several firms have gone into insolvency and more are in financial distress. The move to fixed fee means law firms are now bearing the cost of inefficiency, which they had previously been able to pass on to clients. The results are painful.

In this context, the case for better project management seems overwhelming. A few firms have developed sophisticated approaches. There has been considerable recent press about major firms, such as Dechert, DLA Piper, Eversheds and Latham & Watkins, implementing project management training and software.

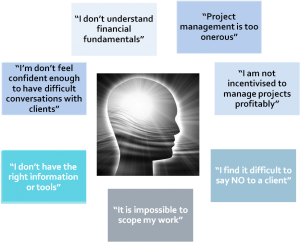

But most firms are struggling to get traction. They are debating what to do, or are struggling to introduce change. So why the slow progress?

The barriers mainly come down to advisers’ mindset. Most partners will buy into the importance of project management as a concept, but are slow to change the way they themselves work. Some see project management techniques as bureaucratic and inappropriate to their highly bespoke work. They are uncomfortable using the new techniques and don’t have the confidence to have frank conversations with the clients about scope (the foundation of good project management). If partners don’t set a visible example, fee-earners won’t follow.

The barriers mainly come down to advisers’ mindset. Most partners will buy into the importance of project management as a concept, but are slow to change the way they themselves work. Some see project management techniques as bureaucratic and inappropriate to their highly bespoke work. They are uncomfortable using the new techniques and don’t have the confidence to have frank conversations with the clients about scope (the foundation of good project management). If partners don’t set a visible example, fee-earners won’t follow.

Learning from the accountants – But there is no need to despair. The good news is that the large accountancy firms have already blazed this trail. Law firms would do well to emulate them. Fifteen years ago they started programmes to improve project management, driven by declining margins in audit and tax work, and the switch from hourly rate to fixed fees. Meridian West interviewed the former managing partner of a law firm who acknowledged that “the accountants have got smarter, much smarter than lawyers [at project management]”. Many of the strategies devised by the large accountancy firms can be directly applied to law firms.

What are these strategies?

Develop simple protocols, don’t invest in complex “project management” software / protocols – Be sensitive to the uniqueness of professional services. Prince 2 and various other methodologies and software programmes developed in the corporate world do not apply well. They are too prescriptive, and too complex. There are horror stories of law firms spending a million pounds on advanced project management software which are hardly used. It is better to work with fee-earners to develop a series of straightforward protocols and templates, adapted to their particular practice area eg dispute resolution, commercial contracts, M&A. In effect, rather than teaching lawyers about theoretical ‘project management’, turn the subject around and capture instead best practice ‘matter management’, which is a subject more likely to grab the practitioner’s attention.

Position the strategy as “profitability management” rather than “project management”. Project management is seen as mundane, whereas all partners understand the importance of profit management.

Help partners become financially literate. Partners need to full understand the economics of the law firm and each project. Partners often have a sketchy understanding of the impact of different pricing mechanisms, charge out rates, leverage, and write offs on profit margin.

Provide real-time financial information. In a recent seminar Meridian West ran on project management, two thirds of attendees acknowledged that they were not able to track project profitability in real time. Indeed the issue is often even worse, with practitioners failing to support the preparation of a budget for fixed fee work, and therefore not having a means of accurately appraising performance on a week-by-week basis. This is a serious shortcoming. Unless fee-earners know if a project is becoming unprofitable, they cannot take actions to put it back on track.

Map how your matters are really managed. Process mapping helps you understand how time is really wasted rather than rely on self-evaluation. This involves reviewing the files of a small number of similar matters (eg litigation, acquisition). In short it is a technique to find out how the business operates to deliver a service: what people do, how they do it, how long they take and in what order.

The exercise enables management to understand.

a. How different is the work that is actually done from that which is laid out in internal guidelines?

b. How different is the work that is actually done from what may be considered industry best practice? Both are critical to then following up with an appropriate and effective process improvement programme.

Training and workshops in isolation are usually ineffective, because few fee-earners really know how much time they spend on each task, or indeed are able to accurately describe what actually happens in practice. Attempts have been made to apply wider industry techniques to process mapping (eg Six Sigma), with mixed results. It is important the review is conducted by people with a strong working knowledge of the legal business, and critically the high value activities.

Use process improvement exercises as an opportunity to enhance “added value” as well as cutting cost. Process mapping is an opportunity to enhance the quality and consistency of the client experience. Over the last 2 years Meridian West has surveyed the views of over a thousand clients of law firms. They want lower prices but they also want better consistency of service and more commercial advice. They are telling us that they want better scoping out of the work, more intelligent delegation, better communication, more transparency on process and more commercial advice. The GC of a FTSE 100 company put it bluntly, “If you guys are charging us £500 an hour, it better be perfect.”

So: good project management is an essential survival tool. But more than that, it is also a significant driver for enhancing the client experience. Without it, you have, inadequate scoping (with possible pricing implications) and major risk of not meeting client expectations. Leading firms are developing methodologies and techniques that enable them to deliver a high quality and consistent quality of service. But even good project management will only get you so far.

The final delivery is judged as much on ‘Commerciality’ – a concept which Meridian in West has refined, having undertaken substantial research on the subject. In essence, Commerciality consists of ‘7 Habits‘, driven by a steady focus on the client’s business goals – ie not just delivering a technically brilliant solution. Combining ‘Commerciality’ with good project management can move you into the sweet spot where you are pricing right and delivering well. As the diagram above shows, the alternative positions are uncomfortable and unsustainable for most firms.

by Ben Kent, John Rowley and Andy Smith